I have been reading recently about other blogger’s strategies when it comes to Lending Club filters. I wanted to write about another technique that I utilize, which is creating filters that are restrictive based on how much you need to keep invested. Having a smaller account means that I don’t need to open up my criteria as much as others do. In the long run, (provided loan availability stays consistent) I should be getting even better returns.

My current filter is pretty similar to Peter’s (Lend Academy) filter 1. I have copied it below, but you can view all of his strategies using the link above.

Estimated ROI: 13.99% (from Nickel Steamroller)

Lending Club Filter 1 on Nickel Steamroller

Loan Grade: D, E, F, G

Inquiries = 0

Public records = 0

Monthly income >= $7,500

Loan purpose: All except other, small business and vacation

This filter is great, but I am able to optimize a similar filter even more while still keeping my projected ROI even higher.

Here is what I have been using recently:

My Lending Club filter on Nickel Steamroller

Loan Grade: D, E, F, G

Inquiries = 0

Public records = 0

Annual income >= $145,000 ($12,083 monthly)

Loan purpose: Debt consolidation only

FICO Range >= 675

Projected ROI: 16.31%

Keep in mind that my filter only includes 426 compared to the original filter that included 4,185 (at time of writing). However, I still believe 426 notes is enough data to use for backtesting. Of course, you will sometimes end up picking up notes like this one:

Sign me up!

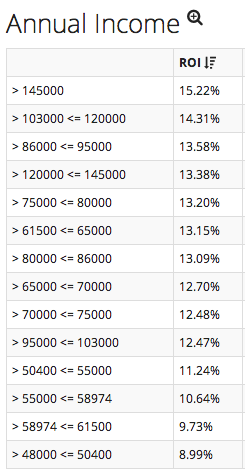

As you can imagine, this note quickly disappeared from my ‘In Review’ Lending Club notes. I think this strategy could be optimized even more as I look closer at what factors increase the projected ROI the most, while still making sure I am viewing enough notes. The best way to do this is to use Nickel Steamroller’s ‘Breakdowns’ section. This can be found under ‘Results Option’ when you are using their back testing functionality. For example. below is the breakdown of annual income on ROI.

Sorted ROI based on annual income

You can see here that annual income does have an affect on ROI. Make sure you keep an eye on the loan ‘Count’ column as there may only be a few loans for a specific income level (or the breakdown you are using). This can skew the projected ROI significantly. To easily visualize the rows you should pay attention to, you can use the ‘Minimum Loan Count’, which can be found under ‘Sub Filtering’ on Nickel Steamroller’s filter page. This will highlight rows based on your minimum selection.

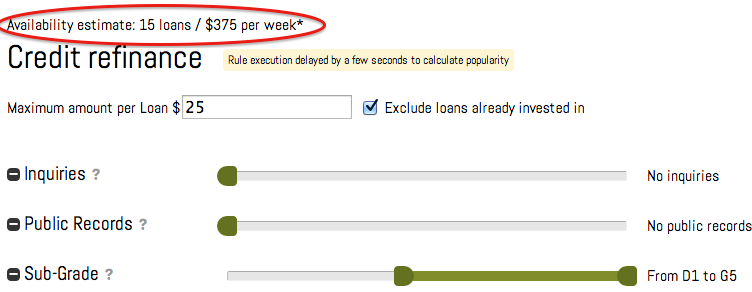

You may be wondering how you will know if you will be able to stay fully invested which your strict filters. One way is to simply set your filter for a week and see what happens. Fortunately, we also have access to the automated investment tool LendingRobot. You can see by the sample filter I have set below that the estimate is 15 loans per week. Keep in mind this is not the same filter as above, I am simply just showing the LendingRobot functionality. According to LendingRobot, “Availability estimates are based on loans made available within the last 2 weeks. Actual investment may vary based on available loans and cash in your account.” In order to see this information, you will need to create an account with LendingRobot.

Do you utilize a similar strategy to try and get the very best notes? Let me know in the comments what you think!

Certainly income is a great predictor of returns for higher interest notes, but the limited availability and competition for notes might make a filter this strict a losing proposition. Considering there have been less than one note per day this year that meets the criteria, anyone with an account over a couple of thousand bucks will have a hard time staying invested as those notes will disappear quickly.

Another factor for consideration is that there isn’t much history for these notes. There have only been 105 36-month notes, and while the default rate looks good, 100 notes isn’t enough to smooth out and accurately predict long-term returns. The bulk of the notes in this filter are 60-month notes, but the average age on those is only 13.4 months. Not very much history for a five year loan.

At any rate, I think filters like this can help gain insight into various credit features, but when they are so limited, it is really difficult to rely on them for any reasonable level of diversification or consistent returns. Thanks for sharing your filter, I look forward to hearing how it works out for you!

W2W, thanks for your comment. I do agree that perhaps relying on data where notes aren’t fully mature may not be ideal. Perhaps I will open the filter up a little bit and choose completed 36 month notes for my projected ROI. I actually have stayed away from 60 month notes for most of my current notes. I still think it’s possible to maximize your ROI in this way, but maybe not exactly with the filter I show above.

As far as note availability goes, I’ve been able to automate the investment of 5 notes from March 1 until March 4. Given that my account of about $7000 produces about $300/month in P & I payments, it looks like I might be able to stay invested, but I don’t have enough data yet to say for sure. (Perhaps the estimates of the notes with these criteria is not 100% accurate.) At any rate, this is why I like being restrictive. If I find that I’m not picking up notes, I can simply loosen up my criteria a little bit. I don’t NEED to make sure I get a note at the next release time, but perhaps later in the day or the next would be fine. It is important to make sure you don’t have idle cash sitting around though.

Automation is absolutely necessary if you want the very best notes that get released.

Logan Thomas says

I’m doing a similar thing myself. I create the filter I want, then increase the monthly income as far as I can while still being able to be fully funded.

Nice! Might as well try to get the very best notes as long as you can stay invested. Thanks for stopping by!