- 1Share

If society can trust technology in self-driving cars, we can trust technology with our finances.

The adoption of technology in the world of money management is a growing trend. More investors are embracing the logic enmeshed in code to create long-term growth. This trust in financial technology, or ‘FinTech,’ fosters a passive environment because investor preferences can be automated without the need for meddlesome oversight.

Furthermore, the passive investing approach is desirable due to its ease and rate of return. In this article, we’ll look at the benefits to a passive investing style and how it applies to the emerging field of peer-to-peer lending platforms like Bondora.

Automation as a Solution to Cognitive Biases

One of the most popular passive investing products today is the robo-advisor, which is a automated service that asks the investor a few questions about their goals and risk tolerance. Next, the interface uses this input to generate investment diversification in a portfolio comprised of asset classes appropriate to the individual. Once the investor sets the parameters, they step back, and their money is poised for gradual growth. This growth is possible because automated investing removes the emotional impulses of the investor whereas active investing burdens the individual with constant well-timed maneuvers to generate returns.

Why is it so important to create a remove from our assets? The field of behavioral economics offers answers by combining cognitive and behavioral psychology to financial markets. The origins of the field belong to researchers Amos Tversky and Daniel Kahneman. In 1979 they authored an article on prospect theory, which endeavors to understand how people misguidedly interpret risk. Their research has lead to a vast body of work revealing numerous cognitive biases that distract us from our goals. A passive investor avoids these pitfalls when the engage in automated investing. Robo-advisors lack these biases.

These flaws in our psychology are often rooted in our tendency to ignore the challenges of analytical, mathematical approaches. This quantitative analysis is where robo-advisors excel. In seconds a program can analyze thousands of data points to synthesize a strategy. With more investment products available than ever before the data is growing and therefore so is the need for efficient analysis.

Passive vs Active Investing

So how has the passive investor performed compared to active investing? Researchers at Morningstar have the answer. In a 2015 publication, they reported the results of their study designed to “measures active managers’ success relative to the actual, net-of-fee performance of passive funds.” The results illustrate that “actively managed funds have generally underperformed their passive counterparts, especially over longer time horizons.” Results like this have popularized the hands-off approach.

These findings are echoed in a similar study that reviewed the performance of 24,000 mutual funds and ETFs for a 10-year period ending on December 31, 2012. The results: “Only 24% of active mutual fund managers outperform the market index.”

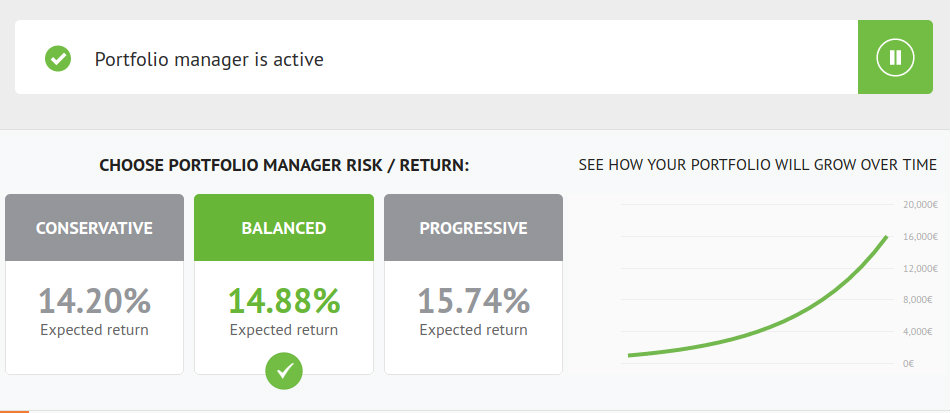

The benefits of automated investing are amplified when coupled with the growing marketplace for peer-to-peer lending. Modern P2P platform Bondora has leveraged passivity to enable the user to generate returns without the burden of endless analysis. Therefore, more investors at Bondora are opting for their Portfolio Manager tool. This system analyzes volumes of data to construct a portfolio matching the conservative, moderate, or progressive risk tolerance of the user.

The automated investing aspect of Bondora’s P2P lending is important because it strikes a balance between risk and return. The result is an optimized portfolio that accepts the least amount of risk possible while achieving the investor’s goal ROI. How does their framework accomplish this? The answer is investment diversification. By spreading the total funds across various borrowers and credit rankings, Bondora’s investors mitigate risk intelligently.

Managing Big Data

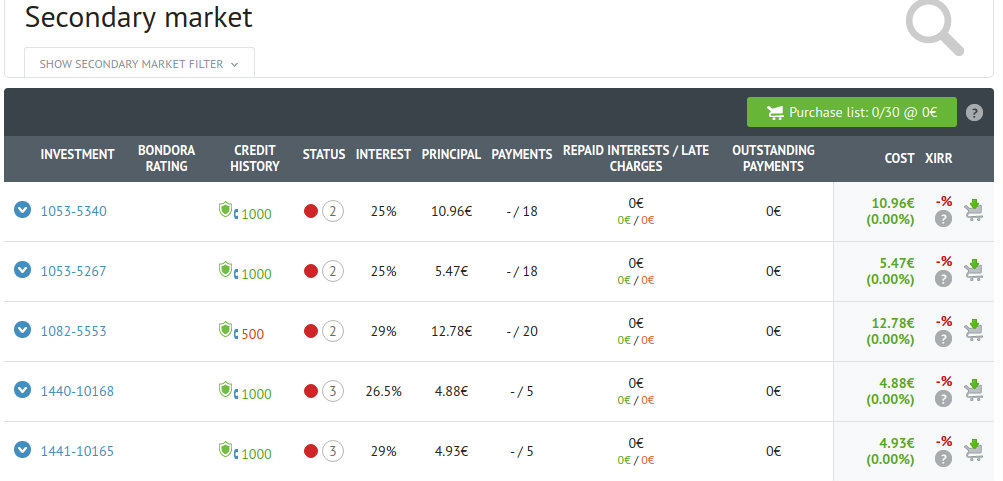

While there are clear benefits to passive investing, those on Bondora’s site that wish to test their investing prowess can do so with the Bondora API system. This tool allows the active investing customer to bid on specific loans based on the nuances of the users goals and risk tolerance. This granular reporting is suited for those who prefer a deeper dive into analytics to achieve a superior return. The world of P2P lending is still developing, and some of those on the ground floor believe they can realize the value of accessible data to beat the market.

Bondora’s Portfolio Manager and API framework are critical to today’s investors because it creates an efficient P2P platform. The result is a more accessible marketplace for lenders and borrowers alike. In under-banked regions more borrowers are turning to peer-to-peer lending. In many cases, borrowers with strong credit are unwilling to withstand the drag and bureaucracy of traditional lending institutions.

Amplifying Returns

On the other side of the transaction investors are turning to P2P lending as an investment product because of a prevailing notion that there will be “more muted returns, if you will, over the next decade” as asserted by Vanguard CEO Bill McNabb. Those wanting to improve this tepid forecast will be attracted to an annualized net return on investment of 16.5% seen on Bondora.

Though the benefits of passive investing are well understood, it is the FinTech industries influence that’s popularizing its adoption in P2P lending. This technological growth emboldens investors to explore the nascent world of marketplace lending. While high investment returns and investment diversification will keep an investor partnered with a company, it’s the ease of investment opportunities that will get them in the door.

Online investing promises greater advances in technology as a primary differentiator among competitors. Ever-increasing efficiencies have driven down many costs. Now, prospective investors are looking to auto investing solutions to carry them to their goals. This automation is the same technological growth that has given rise to the world of marketplace lending. The value of peer to peer lending has always been clear, but technology has made it tangible.

Passive investing has never been more applicable than it is for P2P lending. Auto investments deter cognitive biases which lead us astray, makes unlimited data manageable and minimizing costs. Before painstakingly committing to an active style consider the compounding value of passive investing in the marketplace lending sphere.

- 1Share